Pensions

Whats the first thing that pops into your head when you hear the word pension?

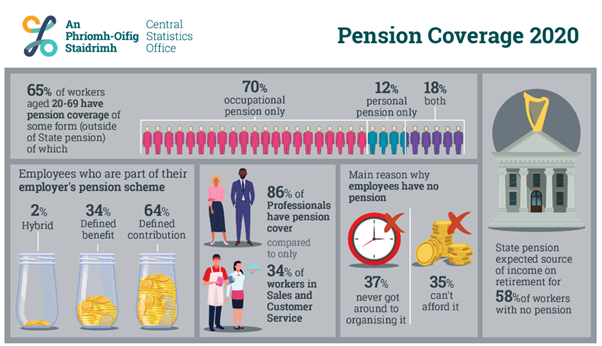

Maybe it is the hassle of setting one up or the thought of getting old, Scary could be a word and certainly some of the trends in the Irish pension market might give you Goosebumps.

What is a pension, it is a savings plan, and it has lots of legislation attached this is what makes them complicated in my honest opinion. The aim of taking out a pension is of course to provide us with an income when we decide to stop work and hopefully, we will all make this decision at some point and enjoy our years that we have left. Thankfully thanks to advances in medical sciences etc we are all living longer and enjoying our retirement years.

So let’s look at how pensions are at the finish rather than at the start. I think it is really important to understand how they work when you retire to understand them better. To break it down the object is to build a fund that you can use for your retirement. While we are building this fund we are entitled to tax relief on our contributions at our own rate of tax

In other words if we are in the 20% tax bracket for every €100 euro we put in our pension we get €20 back and if you are in the 40% bracket for every €100 you put into your pension you will get €40 back.

Now don’t get too excited while this looks great in the early years while we are getting tax relief please remember if something has tax relief it is taxable on the other side. (thanks Government) Lets say Jack has built a pension fund of €250000 in his personal pension and now he is 62 and he has decided to retire. (yes you can retire from 60 on using a personal pension ) you will not receive a state pension until 67 though

Pension fund €250000 Tax free lump sum (please take this) €62500 (Probably only chance ever to get tax free cash !) The balance of €187000 is now used to purchase your pension through two means. One is an annuity this is where you basically sell the €187000 to some provider for a guaranteed monthly pension. These are great if there is decent interest rates which of course we don’t have these days .

One thing to remember once you have sold your pension its sold and there is no going back yes you have a guaranteed income for life but if you have family and you die, they may only get 50% of your monthly payment for five years or ten years depending on the set up so whoever you sold your pension too could do quite well. If you live to a great age you might do well to earn more than the balance of €187000 from the Annuity!

Second option (most popular option) AMRF_ARF Approved Minimum Retirement Fund (Based on today’s pension rules) This fund has to have a minimum of €63500 in it if you do not have a guaranteed income of €12700 per year. In this case you have a fund after your tax free lump sum of €187000 and therefore €63500 must go into this fund. €187000 – €63500 = €123500. What can you do with this fund of €63500 well you can draw 4% per anum from this fund (known as deemed distribution) which equates to €2540 per anum and that’s it really until you reach age 75 at which point you can draw what you wish from it.

This is a yearly payment only and you cannot change it to a monthly payment. There is talks of scrapping this system, but it has to go through legislation, and this is a slow process. Let’s look at the balance after the AMRF this then goes to a ARF so in this case you will have €123500 going into this fund. An ARF stands for an approved retirement fund. But because you will have a guaranteed income of €12700 per year in this case you can skip the AMRF and put the entire €187000 into an ARF

An ARF stands for an approved retirement fund. In this pension vehicle you can draw any amount you want off it . Ideally this ARF will be invested in such a way that your capital of €187000 will not be eroded

What I mean by this is that the drawings you decide to take off this ARF will be outperformed by the growth on this.

What is an AMRF and ARF They are both pension vehicles that you no longer contribute to. You are finished paying regular premiums into these, so they become once off investments as such. Now the ARF you can draw down any amount you decide to draw down on a monthly basis, so this is really your monthly pension. So, on a fund of €123500 you could draw 10% or twenty percent whatever suits you.

So, if you can draw €12350 per year or €1029 per month this would give you a pension of €1029 per month along with €901 per month from the social welfare pension which unfortunately becomes a taxable benefit in the eyes of the state so this is what it would look like.

This amount would be taxable at 20% under today’s rates, there is also talks at the moment that the AMRF-ARF system will be scrapped but at the moment this is just talks and we will have to wait and see in this case so let’s be realistic and work with the figures and facts we have today.

Back to today and how do we start planning for our Pension . While its important to look at the future we also need to plan for it in the best way possible and this is really about the marathon over the sprint

Now the decision is how much do I put into my pension? The Important thing is to start with what you are comfortable with and that you can forget about because once you go in you cannot come back out until you are at least 60.

Now when I say you can’t come out you can of course make these policies paid up, reduce the payments in them and increase the payments in them you can also put once off lump sums into them. The one thing you cannot do is take out the money before you retire. You also have access to a client center where you can see the performance of your funds and you can also do free fund switches within this portal so now days you have a lot more control over your pension.

Over to you guys

Hit the contact button bottom right 🙂

Until Next time Take Joy in the Little Things